Volga Baikal AGRO – USDA WASDE Report October 2020 Information Table !!!

World Agricultural Supply and Demand Estimates.

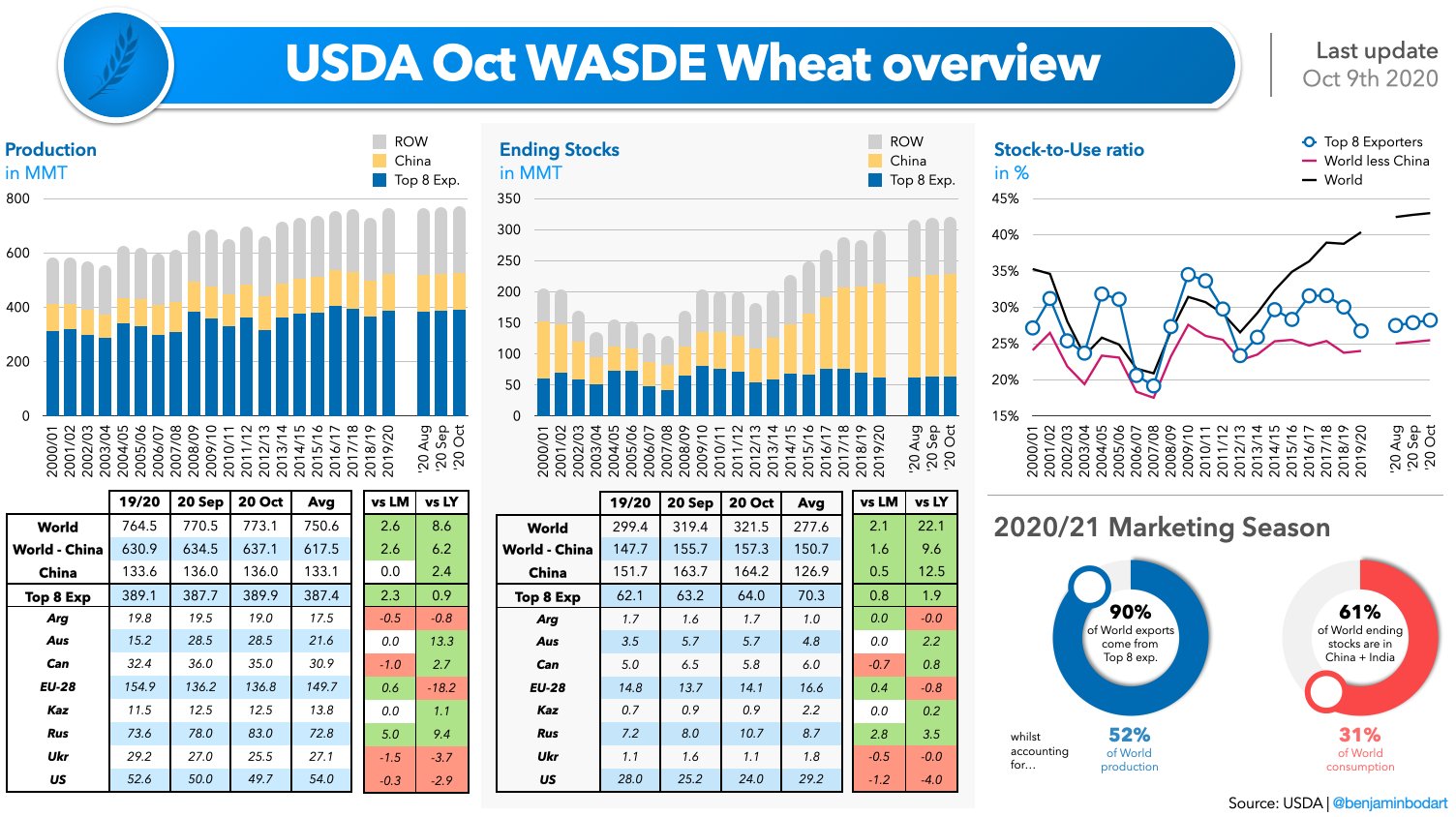

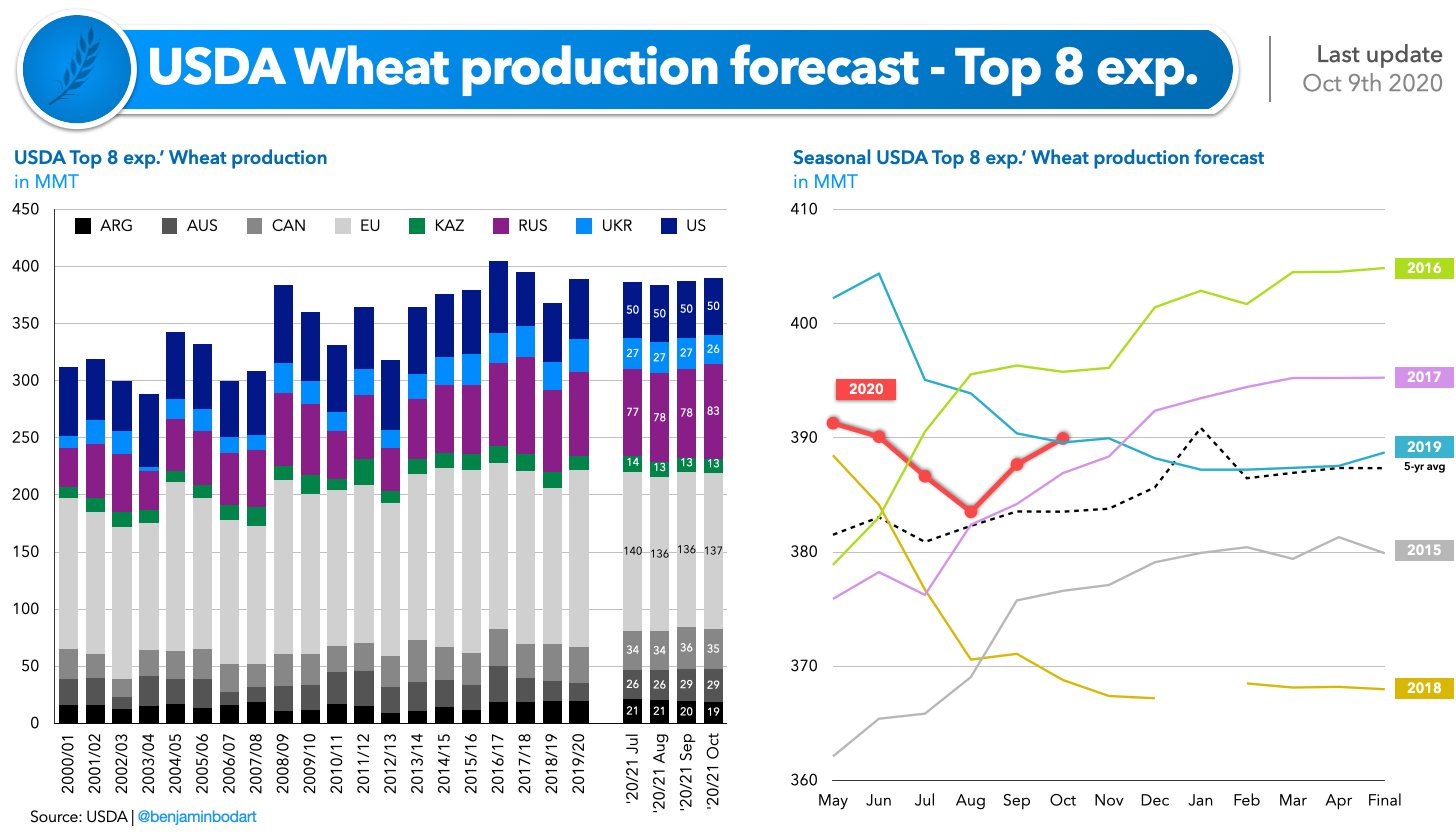

World WHEAT Outlook:

The outlook for 2020/21 U.S. wheat this month is for reduced supplies, higher domestic use, unchanged exports, and lower ending stocks. Supplies are reduced by 32 million bushels, on the combination of lower beginning stocks and production as indicated by the NASS Grains Stocks and Small Grains Annual Summary reports, respectively. Partly offsetting are lower imports, with all the reduction for Durum. Domestic use is raised 10 million bushels, all on higher feed and residual use. The NASS Grain Stocks report indicated greater first quarter disappearance than previously estimated. Exports remain at 975 million bushels due to offsetting by-class changes. Projected ending stocks are reduced by 42 million bushels to 883 million, which would be the lowest ending stocks in six years. The season-average farm price is raised $0.20 per bushel to $4.70 on reported NASS prices to date and expectations for futures and cash prices for the remainder of the marketing year.

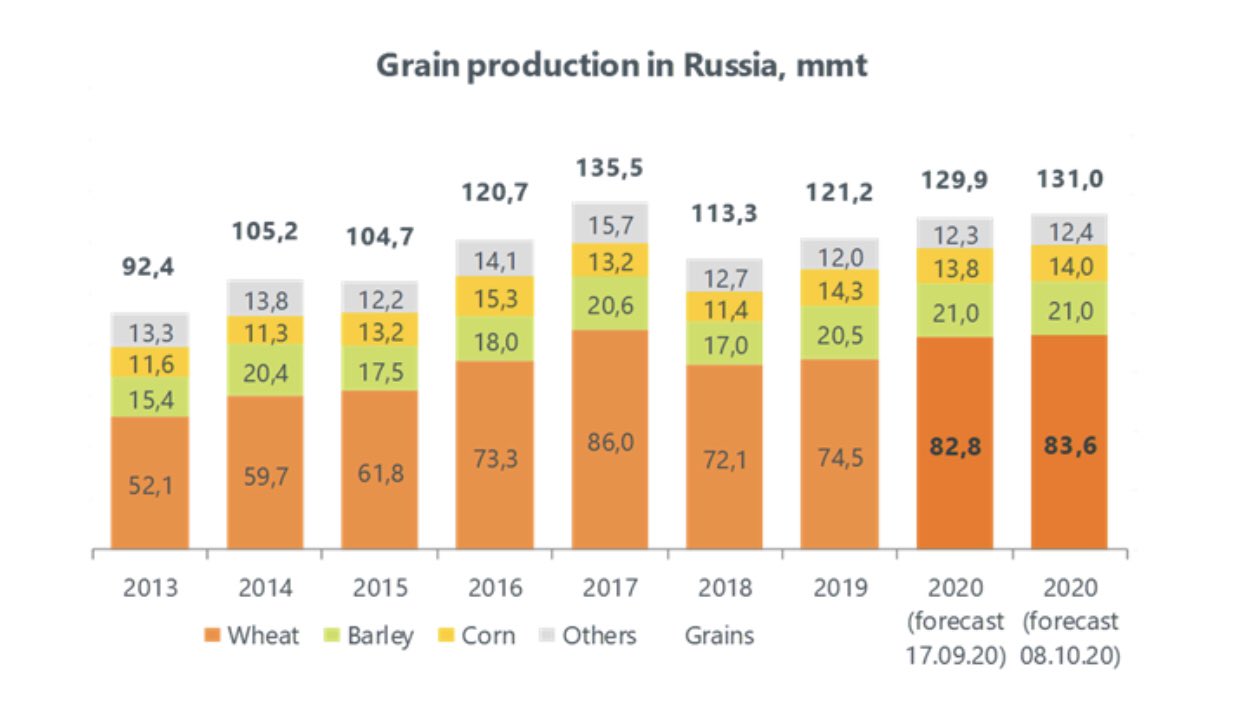

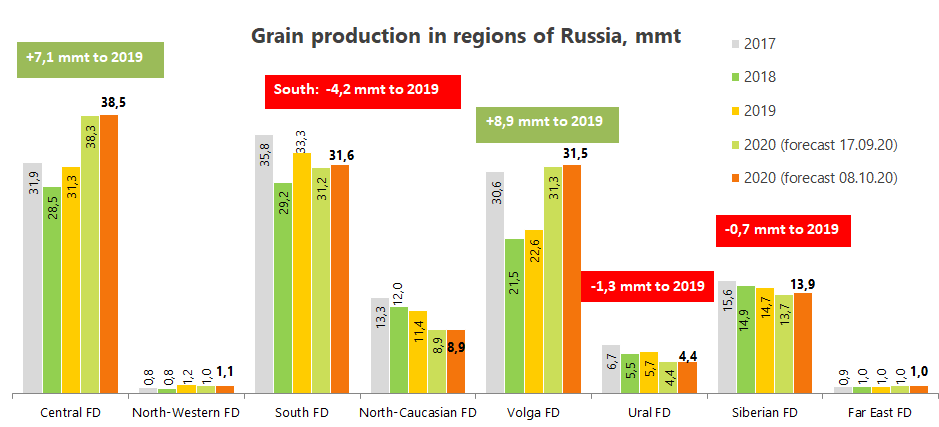

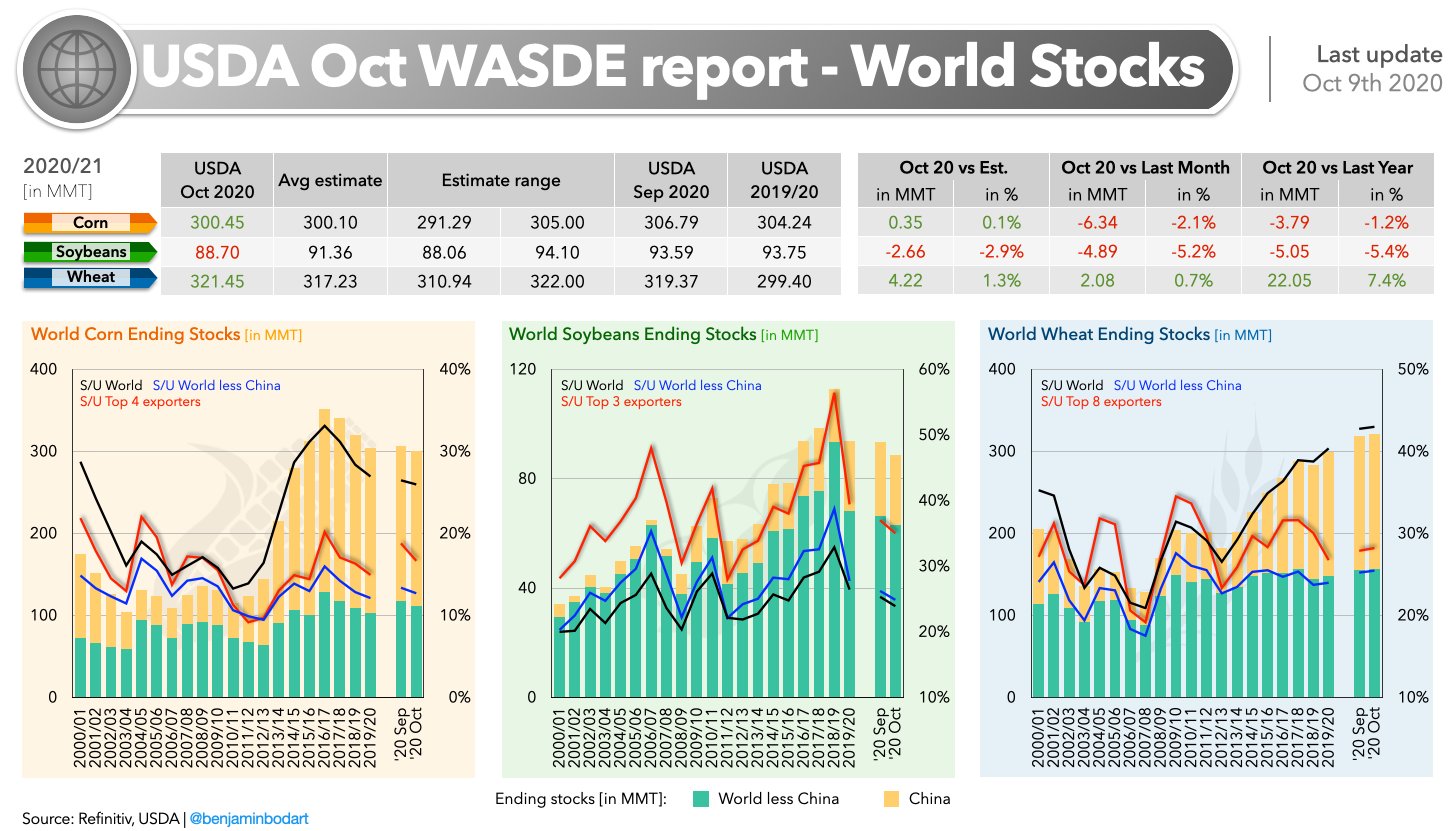

The 2020/21 global wheat outlook is for larger supplies, increased consumption, greater exports, and higher stocks. Supplies are raised 2.2 million tons to 1,072.5 million, mostly on Russia’s production increasing 5.0 million tons to 83.0 million, which is the second-largest crop on record, following 2017/18. The increased production is based on updated harvest results as reported by Russia’s Ministry of Agriculture, which imply record-high spring wheat yields. Russia’s increased production more than offsets reductions in Ukraine, Canada, Argentina, and the United States. Ukraine’s production is lowered 1.5 million tons to 25.5 million, based on Ukraine’s State Statistics Service estimates. Canada’s production is reduced 1.0 million tons to 35.0 million, primarily on the updated Statistics Canada forecast issued September 14. Argentina’s production is lowered 0.5 million tons to 19.0 million on continued dry conditions in some regions. World consumption is increased fractionally to 751.0 million tons, primarily on higher feed and residual usage for Russia and greater food, seed, and industrial use in Pakistan and EU more than offsetting lower feed and residual use for Ukraine and Canada. Projected 2020/21 global trade is raised 0.5 million tons to 189.9 million on higher exports for Russia more than offsetting reductions for Argentina and Ukraine. Russia’s exports are raised 1.5 million tons to 39.0 million, which are the second highest on record. The largest import changes this month are for China and Pakistan, each raised 0.5 million tons. China’s imports are raised on a strong early pace and are now 7.5 million tons, making China the third largest global importer for 2020/21. Pakistan imports are now 1.5 million tons, raising stocks which have been relatively tight recently. Projected 2020/21 world ending stocks are raised 2.1 million tons to

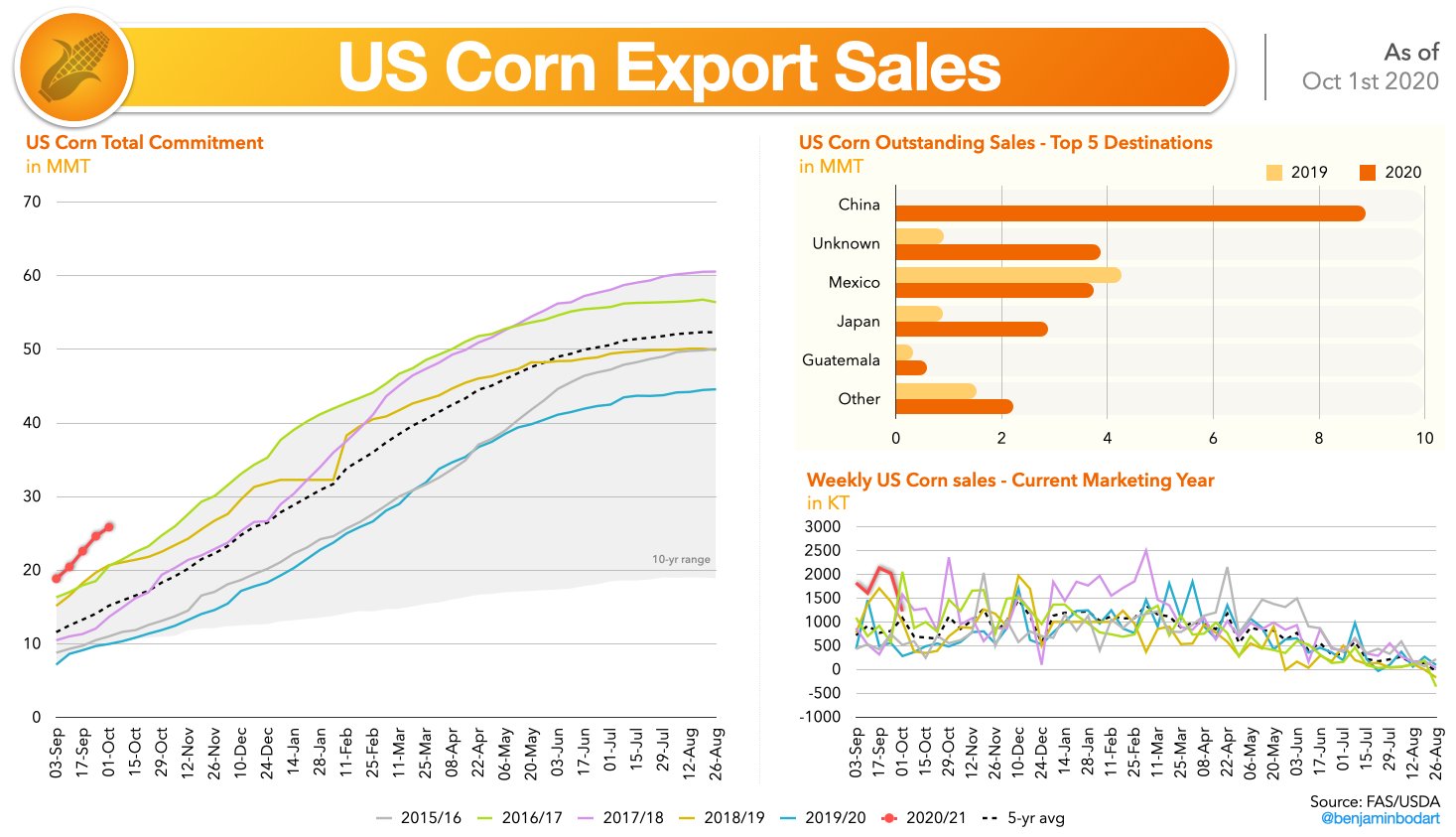

World CORN Outlook:

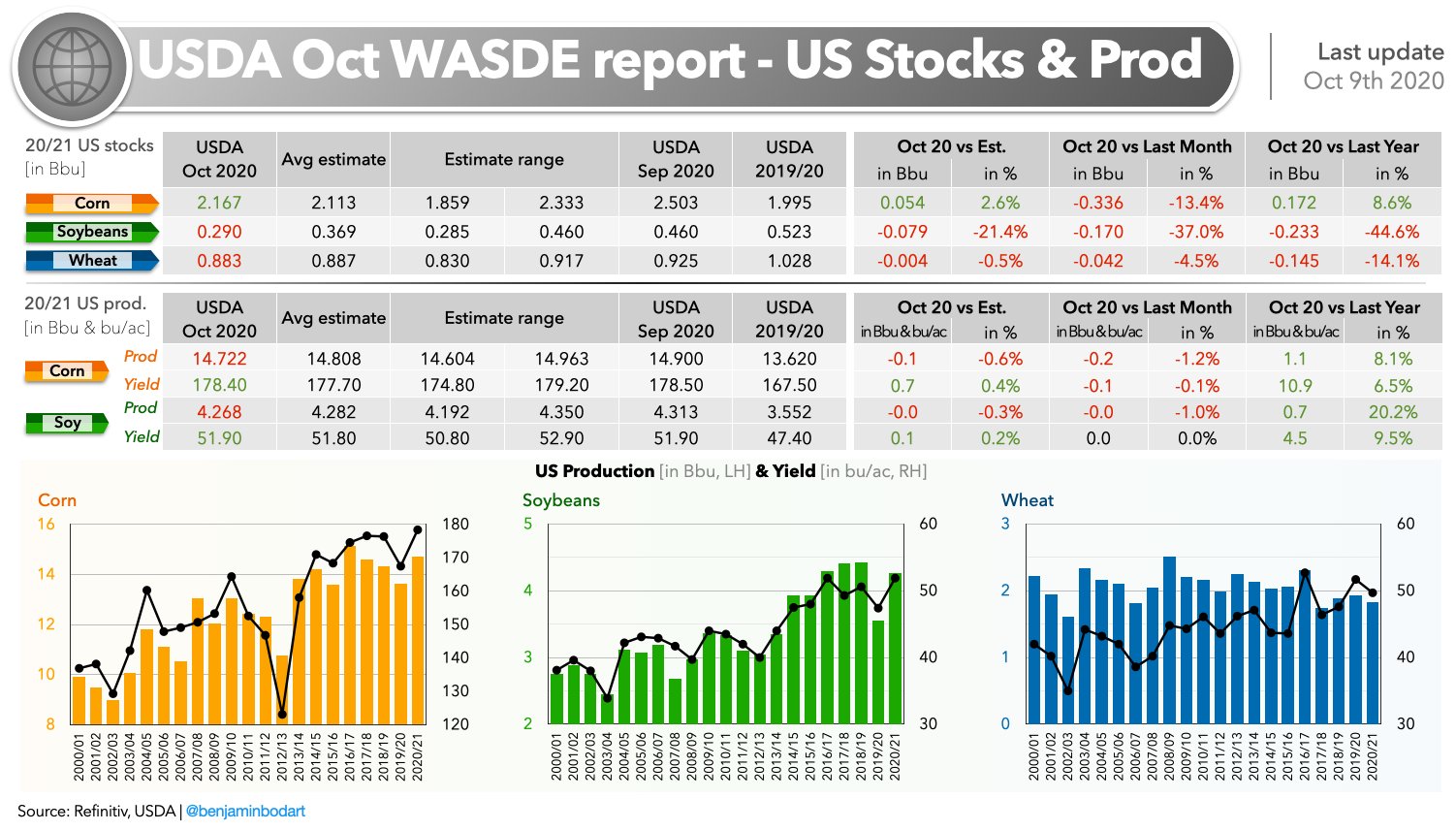

This month’s 2020/21 U.S. corn outlook is for lower production, reduced corn used for ethanol and feed and residual use, and smaller ending stocks. Corn production is forecast at 14.722 billion bushels, down 178 million with a reduction in harvested area and a slight decline in yield to 178.4 bushels per acre. Corn supplies are forecast down sharply from last month, on a smaller crop and lower beginning stocks. Corn used for ethanol is down 50 million bushels, based on weekly ethanol production data as reported by the Energy Information Administration into early October. Projected feed and residual use is lowered 50 million bushels based on a reduced crop and higher expected prices. Corn ending stocks for 2020/21 are lowered 336 million bushels. The corn price is raised 10 cents to $3.60 per bushel.

Grain sorghum production is forecast higher from last month, with a 0.2-bushel per acre increase in the yield to 74.1 bushels per acre and an increase in harvested area.

Global coarse grain production for 2020/21 is forecast lower to 1,458.8 million tons. The 2020/21 foreign coarse grain outlook is for higher production, increased use, and greater stocks relative to last month. Foreign corn production is forecast modestly higher with increases for several countries, including Serbia, Ghana, Kenya, Tanzania, Burkina, and Mali more than offsetting declines for Ukraine and the EU. The projected corn yield for Ukraine is lowered based on reported harvest results to date.

Corn exports are raised for Serbia but lowered for Ukraine and the EU. For 2019/20, corn exports for Argentina are raised for the local marketing year beginning March 2020 based on larger-than-expected shipments through September. For 2020/21, corn imports are lowered for the EU, Iran, and Kenya, but raised for Saudi Arabia, Vietnam, and Iraq. Foreign corn ending stocks are higher, mostly reflecting increases for Mexico, the EU, and Canada. Global corn ending stocks, at 300.5 million tons, are down 6.3 million from last month.

RICE: The outlook for 2020/21 U.S. rice this month is for increased supplies, unchanged domestic use and exports, and higher ending stocks. Supplies are raised as NASS increased the all rice production forecast by 1.3 million cwt to 226.3 million, on higher harvested area and yields. The all rice yield is forecast at 7,567 pounds per acre, up 38 pounds from the previous forecast. Supplies are also increased on higher projected imports, which are raised by 0.5 million cwt to 37.3 million, with all the increase for long grain. This nearly matches last year’s record imports as strong demand for Asian aromatics is expected to continue for 2020/21. Projected 2020/21 all rice ending stocks are raised 1.8 million cwt to 47.7 million, up 66 percent from last year. The projected 2020/21 all rice season-average farm price is raised $0.20 per cwt to $12.80.

The 2020/21 global outlook is for smaller supplies, greater consumption, lower trade, and reduced stocks. Rice supplies are lowered 2.7 million tons to 678.6 million, primarily on reduced beginning stocks for India as its combined 2019/20 consumption and exports are raised 5.0 million tons. India’s consumption is increased on the introduction of government food assistance programs to address economic disruptions caused by COVID-19. India’s exports are raised on its recent robust monthly shipment pace. World production for 2020/21 is raised 1.9 million tons to a record 501.5 million, mainly on higher projected output for India and the Philippines. Global 2020/21 consumption is raised by 3.0 million tons to a record 499.4 million, primarily on increases for India and Thailand. World trade is decreased 0.2 million tons to 44.3 million tons as higher exports for India are more than offset by reductions for Thailand and Pakistan. Projected 2020/21 world ending stocks are lowered 5.7 million tons to 179.2 million, still a record, with China and India accounting for 65 and 18 percent of the total, respectively.

World SOYBEAN Outlook:

U.S. oilseed production for 2020/21 is projected at 126.6 million tons, down 1.1 million from last month with lower soybean, peanut, and cottonseed production partly offset with higher canola and sunflowerseed. Soybean production is forecast at 4.3 billion bushels, down 45 million on lower harvested area. Harvested area is reduced 0.7 million acres to 82.3 million, with reductions for Kansas, North Dakota, and South Dakota. The soybean yield is projected at 51.9 bushels per acre, unchanged from the September forecast. Soybean supplies for 2020/21 are forecast at 4.8 billion bushels, down 96 million on lower production and beginning stocks. Despite reduced supplies, soybean exports are raised 75 million bushels on record early-season sales. With smaller supplies and increased exports, ending stocks are projected at 290 million bushels, down 170 million from last month.

The U.S. season-average soybean price for 2020/21 is forecast at $9.80 per bushel, up 55 cents reflecting smaller supplies and higher exports. The soybean meal price is forecast at $335.00 per short ton, up $20.00. The soybean oil price forecast is raised 0.5 cents to 32.5 cents per pound.

The 2020/21 foreign oilseed production is lowered 2.6 million tons to 478.9 million mainly on lower sunflowerseed production for Ukraine, the EU, Moldova, and Argentina. Ukraine’s sunflowerseed output is lowered 2 million tons to 15 million on drought conditions during the season and harvest results to date. Dryness also impacted yield prospects for Romania, Bulgaria, and Moldova. Lower sunflowerseed production for Ukraine results in lower global sunflower meal and oil exports. Partly offsetting are higher exports of palm oil from Malaysia and rapeseed meal from Russia.

The 2020/21 foreign soybean supply and demand forecasts include lower beginning stocks, higher crush, and lower ending stocks. Beginning stocks are lowered mainly on higher 2019/20 crush for China that is partly offset by lower exports and higher stocks for Brazil. The 2020/21 soybean imports, crush, and meal consumption are higher for China, Bangladesh, Thailand, and Vietnam, aligning with prior year increases in domestic meal use. Argentina’s exports are lowered 0.5 million tons due to stronger competition from the United States. With lower supplies in the United States and higher foreign use, global ending stocks are reduced 4.9 million tons to 88.7 million.

World Agricultural Supply and Demand Overall Estimates.:

Report Link: USDA WASDE Report October 2020…………………………..

Report Link: USDA Grains Report October 2020……………………………

Report Link: USDA Oilseeds Report October 2020………………………….

Report Link: USDA World Production Report October 2020…………….